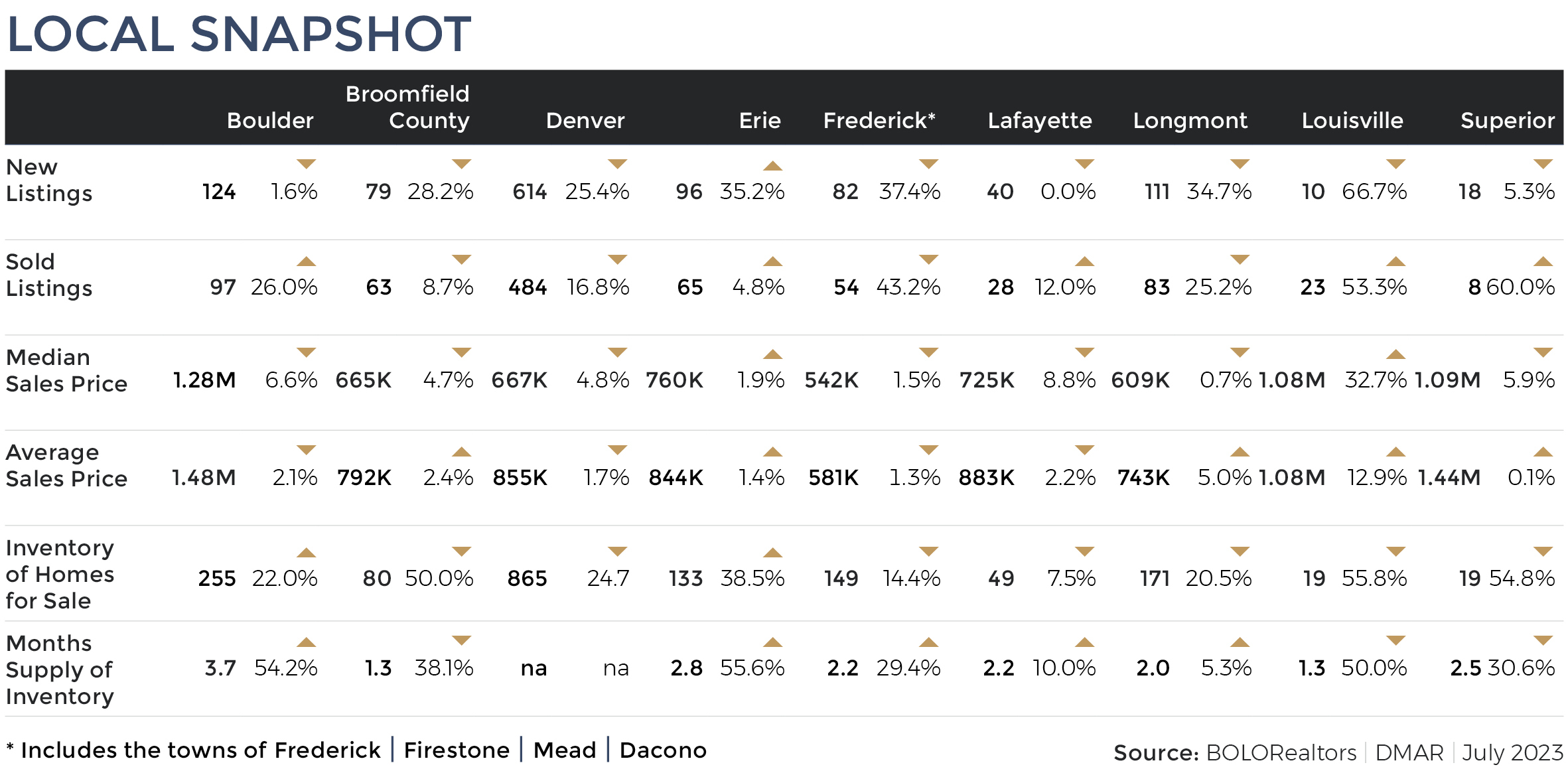

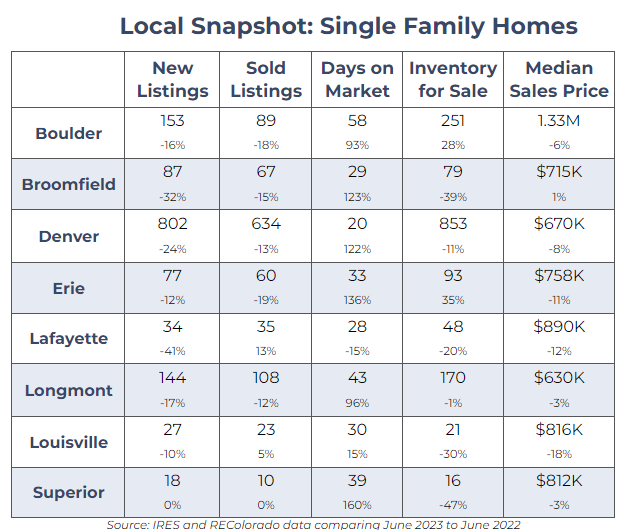

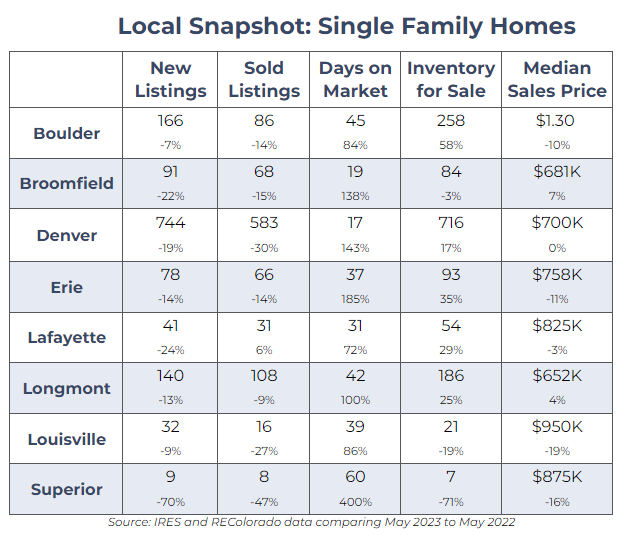

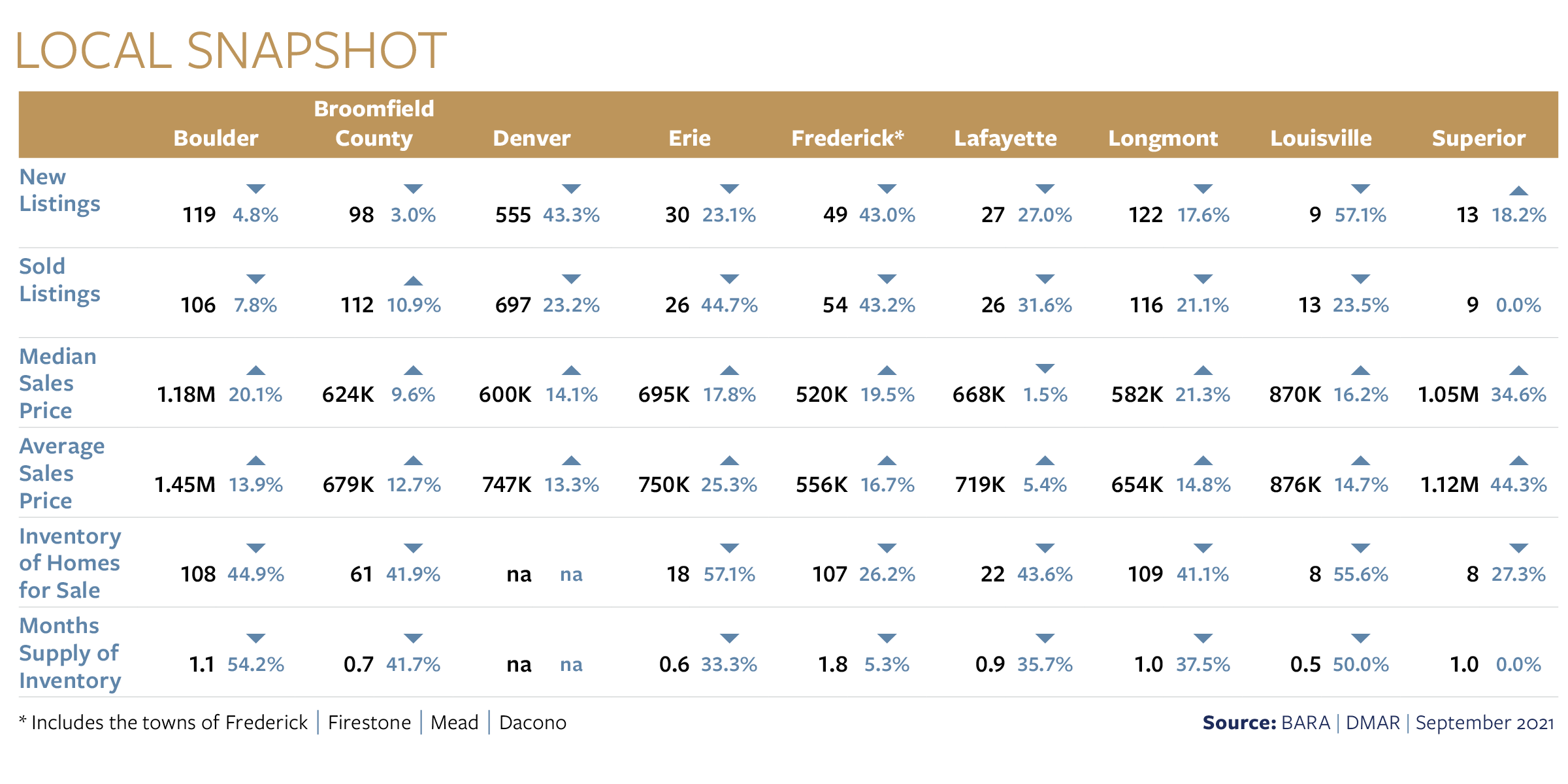

News to Know This Month

Where are all the showings? This is the most common question I’m hearing from sellers right now. The home is priced well, the condition is great, but the total number of showings are lacking that frenzied back-to-back showing schedule we saw previously.

And that’s okay.

It only takes one serious buyer and showing to sell a house, and I can assure you buyers are still out there. However, we are in a market where we need to be patient and confident that a home will sell, it just may take longer overall with showings spread out over a period of time.

Buyers, this doesn’t mean you can necessary get a home for significantly under asking price, as many sellers know the worth of their home and aren’t willing to take a low offer. However, this does mean there is typically room for more negotiation. The most common trend I’m seeing is sellers offering concessions that can be used to buy down an interest rate or be used toward closing costs. This can lessen the total amount of cash you’ll need to bring to the closing table.

As always, let me know if I can offer any assistance with your real estate needs!

~Andria Allen

303-810-8375

Corn Mazes and Pumpkin Patches

Your guide to corn mazes and pumpkin patches along the Front Range is here, complete with an interactive map…Read More

20 Questions to Ask When Selling a House

Thinking about selling soon? Here are 20 questions to ask your real estate agent as you prepare to sell your home…Read More